Taxes

Room found for priority tax cuts despite overall tax rise

Government revenues are forecast to be £670.3 billion in 2015-16. That is 35.5% of national income, the same as in 2009–10, despite the net effect of policy measures implemented by the coalition government being to increase taxes.

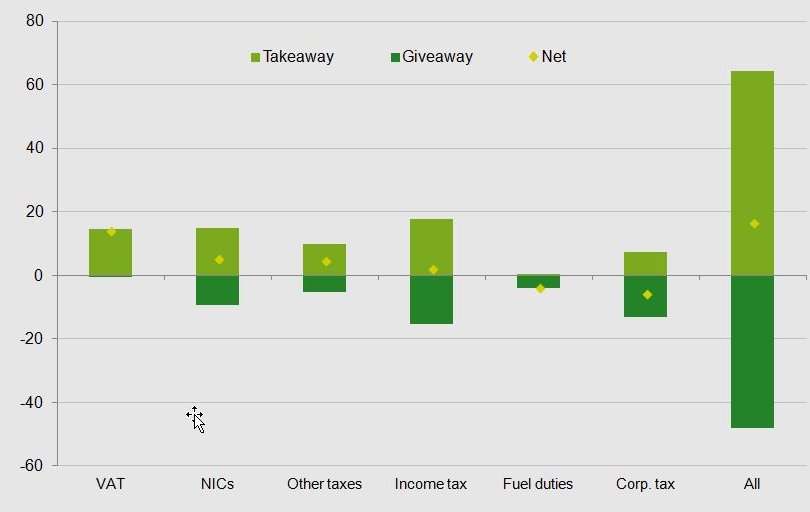

Figure 1: Revenue effects of tax changes implemented by the coalition [get the data for the graph]

Source: Authors’ calculations based on the Office for Budget Responsibility’s Policy Measures Database April 2014 and various Budgets, Autumn Statements and Pre-Budget Reports.

While the emphasis of the coalition’s deficit reduction plans has been on spending cuts, the overall direct impact of tax changes is also to reduce borrowing, by £16.4 billion in 2015–16: the net effect of £64.3 billion of tax rises and £48.0 billion of tax cuts. The biggest tax increases were implemented early in the Parliament: a rise in the main rate of VAT from 17.5% to 20%, a sharp reduction in the amount that can be saved in tax-privileged pensions, and a 1 percentage point increase in all rates of National Insurance contributions (NICs) that had been announced by the previous Labour government. All of these exacerbate unwelcome distortions in the tax system. The first increases the distortion towards buying VAT exempt, reduced- or zero-rated goods and services, the second reduces the coherence of the taxation of pensions, and the third increases the existing incentive to shift the form in which income is taken away from earnings and towards capital income. A steady stream of smaller reforms and anti-avoidance and anti-evasion measures has also made a sizeable contribution to raising revenues, particularly income tax revenues.

Despite the overall tax increase, however, the government has managed to find scope for three big tax cuts. Foremost among these is the increase in the income tax personal allowance to £10,600 in 2015–16. This primarily benefits working-age families in the upper half of the income distribution – few of the poorest families contain a taxpayer while two-earner couples, who tend to have higher family incomes, benefit twice over from the increase – though reductions in the higher-rate threshold have taken money away from higher-rate taxpayers. Taken together, changes to the personal allowance and the higher-rate threshold implemented by the coalition have a net cost of £8.0 billion. Another area of priority for the coalition has been reducing the main rate of corporation tax, which has fallen from 28% in 2010-11 to 20% by 2015–16 at a cost of £7.6 billion. Both of these priorities were clearly signalled by the coalition when it took office. Not signalled in advance was a series of announcements of real-terms cuts to fuel duties, which in April 2015 will be 15% lower than if the April 2010 duty had simply been uprated in line with the retail prices index, a £3.9 billion tax cut.

As we set out in an IFS Election Briefing Note, most of the coalition’s other tax reforms have also involved simply changing rates and thresholds, with little attempt to address the fundamental structural deficiencies of the tax system. Council tax has been cut but allowed to get ever more out of date. Inheritance tax has been increased but its loopholes untouched. Business rates have been cut but made more unstable and continue to discourage property-intensive production. Capital gains tax has been increased but with no clear strategy for dealing with the tension between minimising disincentives to save and minimising avoidance opportunities.

There have been some welcome structural reforms, but even there the job is incomplete:

- Stamp duty land tax no longer has big jumps in liabilities at price thresholds for housing, but still does have them for non-residential properties, and the more fundamental problems with the tax remain.

- The use of the discredited retail prices index to adjust the system for inflation has been ended for direct taxes, but not for indirect taxes. More problematically, an increasing number of thresholds are not uprated at all.

All in all the coalition’s changes represents a missed opportunity to improve the tax system. One possible reason for optimism about the future is that the coalition has made some admirable improvements to the institutions of tax policy–making, enhancing transparency and allowing better scrutiny. That optimism should be tempered, though, by the way in which the coalition has announced tax policy itself. Some areas, such as fuel duties and business rates, have seen a stream of ad hoc, often temporary, announcements overtaking each other without a clear statement of principles or long-run intentions. Arguably, the ad hoc and inconsistent approach being taken to devolution of tax-setting powers to different parts of the UK creates similar uncertainty.

All three main political parties are committed to further fiscal consolidation over the next parliament, and tax rises have historically tended to follow elections . How much (if at all) tax rises should contribute to reducing the budget deficit will be a central question for the incoming government. So too will be the design of any tax increase: how the government chooses to raise a given amount of additional revenue affects both the distribution of the tax burden across the population and the pattern of economic activity. In the 2015 Green Budget, IFS researchers analysed a variety of options the next government might consider to increase tax revenues.

IFS election 2015 publications

Briefing notes

Stuart Adam, James Browne, Carl Emmerson, Andrew Hood, Paul Johnson, Robert Joyce, Helen Miller, David Phillips, Thomas Pope and Barra Roantree, 'Taxes and benefits: the parties' plans', Institute for Fiscal Studies: 28 April 2015, IFS briefing note BN172, election briefing note 2015 No. 13, ISBN: 978-1-909463-90-5

Stuart Adam and Barra Roantree, 'The coalition government’s record on tax', Institute for Fiscal Studies:13 March 2015, IFS briefing note BN167, election briefing note 2015 No. 9, ISBN: 978-1-909463-84-4

Helen Miller and Thomas Pope, 'Corporation tax changes and challenges', Institute for Fiscal Studies: 26 February 2015, IFS briefing note BN163, election briefing note 2015 No. 5, ISBN: 978-1-909463-76-9

James Browne and William Elming, 'The effect of the coalition’s tax and benefit changes on household incomes and work incentives', Institute for Fiscal Studies: 23 January 2015, IFS briefing note BN159, election briefing note 2015 No. 2, ISBN: 978-1-909463-73-8

The 2015 IFS Green Budget

Stuart Adam and Barra Roantree, Options for increasing tax, The 2015 IFS Green Budget, Carl Emmerson, Paul Johnson and Robert Joyce (eds.), February 2015

Observations

Stuart Adam, Unknown quantities: Labour’s ‘non-dom’ proposal, Institute for Fiscal Studies: 9 April 2015, Observation

Stuart Adam and Barra Roantree, Taxes up, taxes down, but fundamental problems unaddressed, Institute for Fiscal Studies: 13 March 2015, Observation

Carl Emmerson and Gemma Tetlow, Labour's proposed pensions takeaway, Institute for Fiscal Studies: 27 February 2015, Observation

Useful resources

A presentation given at the IFS Budget briefing 2015 looked at the implications of Budget announcements for pensions, savings and business taxation.

This briefing note provides an overview of the UK tax system; current and historical rates and thresholds for the main taxes can be found here, while the main announcements on tax in each Budget and Autumn Statement are listed here.

IFS analysis of the measures announced in each Budget and Autumn Statement can be found here.

IFS researchers have also written Observations with further discussion of the introduction of a transferable income tax allowance, withdrawal of child benefit from those with high incomes, reforms to inheritance tax, and Labour’s proposed re-introduction of 10% starting rate and a 50% top rate of income tax.